When you are almost at the end of your house-buying journey, you will become familiar with two terms that are used by your estate agent and conveyancer: exchange and completion.

If you’re a first-time buyer, it might be that you don’t know what these terms mean. It might also be the case that you have moved house before but have forgotten what happens between the exchange and completion stages.

In this guide, we will tell you everything you need to know so keep reading if you’re interested in learning more.

A quick summary of ‘Exchange’

Exchange refers to the ‘exchange of contracts.’ At this point in the house-buying process, the property transaction becomes legally binding so you are contractually obliged to finalise the purchase or sale of the home on the scheduled completion date.

What is the exchange of contracts process?

Below we take a look at what happens both before and during the exchange of contracts.

Before exchange:

- A survey of the property is completed – Learn about property valuation surveys

- The buyer receives a mortgage offer from the mortgage lender

- The seller gathers up the paperwork for their home

- The buyer and seller sign the contracts needed for the transaction and send them back to their solicitors

At the exchange of contracts

- Each solicitor possesses a signed contract

- The buyer’s solicitor is in possession of the deposit, the mortgage offer, and the building insurance policy (if this has been required)

- The seller’s solicitor is in possession of the signed title deeds

- The buyer and seller agree on a completion date

- The timeframe of the house sale is confirmed across the property chain

- The buyer’s solicitor will call the seller’s solicitor and agree to the exchange of contracts

- In the case of a leasehold property, the freeholder will be given the new owner’s details

What is the significance of exchanging contracts?

The day when contracts have been exchanged is very significant because:

- The buyer and seller are legally bound to go ahead with the transaction

- The completion date is set

- The buyer pays monies owed to the seller

- Any party that backs out of the transaction after exchanging contracts will face financial penalties

- After the solicitors have exchanged contracts, the buyer and seller can organise their get respective house moves

A quick summary of ‘Completion’

Completion refers to the ‘completion date,’ the day when the property legally changes hands.

What is completion?

- Completion is the final phase of the property sale

- Property ownership transfers from the seller to the buyer

What happens on completion day?

- The purchase price of the property is paid, minus the deposit

- On receipt of funds, the seller’s solicitor will confirm to their client, buyer’s conveyancer, and estate agent that the sale has been confirmed

- The property is vacated by the seller at the agreed time

- The buyer collects the keys from the selling agent and moves into their new home

- The buyer becomes liable to pay Stamp Duty Land Tax to the HMRC

- The buyer’s conveyancer registers ownership of the property with the Land Registry

What is the significance of completion?

Completion day is very significant because this is the day when both the buyer and the seller begin the next chapter of their lives. The seller moves on to their next property and the buyer takes ownership of the property that has now been vacated.

Exchange to completion in 10 bite-sized steps

Discover the crucial steps that take place between exchange and completion of a property sale with our helpful infographic.

Agreeing on your completion date during the exchange of contracts

The completion date is usually four weeks after the exchange of contracts but this can be negotiated to suit the parties involved.

Before agreeing to a date, you need to:

- Check the prices and availability of local removal companies

- Talk to your employer about booking time off work

- Figure out which day of the week suits the members of your family

When you have agreed on a date with either the buyer or seller, you then need to:

- Book a removal company

- Contact your broadband suppliers and utility companies to let them know your moving date

- Organise buildings insurance

- Inform friends and family of your change of address

- Arrange to have your mail forwarded by Royal Mail

- Book time off work

Why do people complete on a Friday and can you choose another day?

Most buyers complete on a Friday as they have the weekend to unpack and organise their new home, so have little need to book an extra day off work.

But because Friday is so popular, you will need to make a tentative booking with a removal company when you have an inkling of when the completion date might be. Most companies are happy to pencil in a date although this will only be finalised when you have paid them a deposit.

Of course, you don’t have to choose a Friday. If you’re able to book a few days off work, you might want to move into your new property earlier in the week. This will give you more time to unpack your boxes and organise your new home. As mortgage lenders and removal companies are less busy on other weekdays, this is another reason to choose a different day.

Unfortunately, weekends are out of the question so don’t expect to move on a Saturday or Sunday. This is because both the buyer’s and seller’s solicitors need to be available on the completion date and they are unlikely to work at the weekend.

Another reason to avoid a weekend is bank transfers. They don’t go through on a weekend so a weekday is better if you want to avoid delays during the exchange and completion stages.

What happens to the buyer’s deposit on exchange of contracts?

When the buyer exchanges contracts with the seller, they need to pay an exchange deposit.

This deposit is usually between 5-10% of the property’s purchase price. –

Along with the legally binding contract, the deposit is a confirmation that the buyer is committed to the purchase of the property. Should they pull out of the deal after exchanging contracts, they could be sued by the seller and forced to award them compensation (which will include the deposit).

To ensure the transaction process goes smoothly, you should send deposit funds over to your solicitor several days before the exchange date. This can be done via a bank transfer, money order, cashier’s cheque, or cheque that has been cleared by your bank.

Deposits in a chain

The deposit sent by the buyer will usually be used by the seller to pay the costs associated with their next home. They might put the buyer’s deposit towards their own deposit, for example.

So, if Buyer A, at the bottom end of the property chain, was buying a house for £150,000, and they owed the seller (Buyer B) 10% deposit of the purchase price, they would send £15,000 to Buyer B via their solicitor.

On receipt of the deposit, Buyer B could put this money towards the deposit for their next property. If the property cost £250,000 and they needed a deposit of 10%, they would only need to pay £10,000 as the money sent to them by Buyer A could be used to pay the remainder.

Peace of mind for sellers

If you’re a seller, the deposit paid by the buyer can give you peace of mind that they are committed to buying your property. If they back out before the agreed completion date, you will be entitled to compensation, which will include the exchange of contract deposit they have already paid you.

Unfortunately, you aren’t able to access the deposit funds, until after the transaction has been completed. The only exception is if you are buying a new build property as the developer may require the contract deposit at an early stage. In this situation, the funds would be sent over to them and guaranteed by a New Build Guarantee Scheme.

What happens if my deposit is in an individual savings account (ISA)?

There are many ISA’s but the two main ISAs for buying a property are the help to buy ISA and the Lifetime ISA (LISA).

Help-to-buy ISA

A Help-To-Buy ISA can be used to buy a home worth up to £250,000 (or up to £450,000 if buying a property in London). Although many people have an active Help To Buy ISA (Help To Buy Equity Loan Scheme), the government have now closed to any new applicants.

If you already opened a Help to Buy ISA before the cut-off on 30th November 2019, then congratulations – you have until 2029 to continue saving and receive your 25% government bonus by 2030! Don’t miss out on this opportunity to get more bang for your buck.

The money can be used towards the exchange deposit but you will need to request a closing statement from your ISA provider before you can withdraw your saved funds.

You then pass the closing statement to your solicitor, who will claim your 25% bonus from the government. This bonus can be put towards the deposit.

Lifetime ISA (LISA)

The next best ISA for saving to buy a property in the UK is the Lifetime ISA (LISA). This type of individual savings account became available in April 2017 and is engineered to help people save up for the long-term goals of home ownership or retirement. LISAs have proved invaluable resources for many savers since their emergence; don’t miss out on this opportunity!

With a LISA, the government will happily provide an astonishing 25% bonus to your savings every year – this is up to a maximum of £1,000 and completely tax-free! And it doesn’t stop there; you get all these rewards until you reach age 50.

Am I eligible?

If you’re between the ages of 18 and 39, you are eligible for a LISA. Contributions can only be made until age 50; however, after that point, your money can be used to buy your first home (up to £450,000) or taken out at 60 with no penalties imposed. If withdrawal occurs before reaching 60 years old though, 25% will be deducted from the total amount removed.

The lifetime ISA is an excellent choice for those hoping to save up for a first home or retirement and are willing to commit their funds long-term. This option has been proven advantageous time and again due to its attractive savings rate.

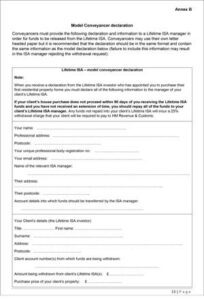

What your solicitor must send the ISA manager

If you are looking to access funds from your Lifetime ISA for a purchase, make sure that you supply the necessary information to the associated manager:

- a declaration that they’re an eligible conveyancer

- a declaration that they have received the information from the LISA holder and that they have no basis to doubt its accuracy and integrity.

- the purchase price of the property

- a declaration to only disburse the amount withdrawn towards fulfilling the cost of purchasing the property.

- details of your LISA account which will be receiving the withdrawn funds

- the solicitor’s unique professional body registration number

- a declaration that having carefully examined the facts and figures, they hereby attest that all of the information provided is accurate and complete to their best knowledge.

Each LISA manager or bank will have their own declination example. Below is a declaration example with text that must be used.

What the bank or ISA manager should do

The ISA Manager is required to transfer funds of the specified amount within 30 days of receiving your declaration.

The charge-free withdrawal will not be approved if:

- The ISA manager has sufficient grounds to assume that the information you provided is inaccurate or incomplete.

- If the first payment to that account is within 12 months of the withdrawal

When the purchase is complete

Within 10 business days of purchasing, your solicitor must inform the ISA Manager via email or post about:

- the completion date of the purchase

- The account number associated with the Lifetime ISA from whence the withdrawal transpired.

- their personalised conveyancer reference number should be registered with the relevant professional organisation.

Read more information on what to do if the purchase failed or isn’t completed within 90 days.

Can you do building work between exchange and completion?

If you need to carry out building work on your new property between the exchange and completion stages, your conveyancing solicitor can request access via a legal document known as a ‘Key Undertaking.’

You should specify what type of work you need to be carried out in a draft. Once this has been agreed upon, you sign the document and make it legally binding. If you breach the terms of the agreement, i.e. by carrying out unauthorised work on the property, you may be sued by the seller.

Can I exchange and complete on the same day?

Yes, it’s certainly possible to exchange and complete on the same day, although most mortgage lenders won’t allow this.

Exchange and completion on the same day usually occur in situations where there is a cash buyer, no chain involved, and the buyer and seller want to make a quick transaction.

In all other instances, it’s quite rare that exchange and completion happen on the same day. This is because:

- Most mortgage lenders require a minimum period (usually five working days) before exchange and completion as it can take a minimum of 48 hrs for the mortgage funds to be drawn down.

- The transaction can become stressful as a lot of work is required for everything to happen on a single day

- A lot can go wrong, such as a delayed transfer of mortgage funds or the risk of signed paperwork not being received on time

As such, it’s better to leave a few days’ gap between exchange and completion to alleviate the stress of everybody involved and to minimise the risk of anything going wrong.

Pros & cons of attending the exchange of contracts

An ‘attended exchange of contracts’ is the term used when a buyer and seller meet in person, along with their respective solicitors, to quickly complete the property deal.

Why do it?

There are a number of reasons why the buyer and seller might want to quicken the property transfer, as we describe below.

- You’re a buyer wanting to purchase a highly desirable property before another buyer gets their foot in the door

- You’re a developer that has a strong interest in the available property

- You’re a cash buyer who is in a position to buy the property immediately without the help of a mortgage company

- You’re a seller with an urgent need to release cash from the sale of your property

How it’s done

- All the parties involved meet face-to-face on the same day (usually at the offices of the seller’s solicitor)

- Both sides work through the sales papers

- An agreement is made and the exchange occurs

If one of the parties can’t attend in person, they make themselves contactable by phone.

Pros & cons

These include:

Pros of attending the exchange of contracts

- The seller can benefit from the proceeds of the sale

- The seller doesn’t have to wait for another buyer

- The buyer can purchase the property before they are gazumped

- Negotiations are straightforward as both the buyer and the seller are in the same room (in person or on the phone)

- Superficial issues can be resolved quickly

Cons of attending exchange of contracts

- As there is no time for a property survey, the buyer might regret the decision to purchase the property if they later discover issues in the house

- Less time to arrange buildings insurance, removals, etc.

- Conveyancing costs are more expensive

Can you pull out after the contracts exchange?

After exchanging contracts, the buyers and seller are legally bound to complete the sale. It’s still possible to pull out of the deal after this point but as this would be a breach of contract, the buyer or seller would face losing your deposit money.

Advice for buyers

If you pull out of the transaction after you exchange contracts, you will lose your deposit and you may have to pay interest on the unpaid purchase price and conveyancing fees.

As such, it’s wise not to exchange contracts unless you are sure you want to go ahead with the property purchase. If you have any doubts at all, hold off until you are satisfied that the property meets your financial and personal needs.

Advice for sellers

If you pull out of the sale after the exchange date, you are liable to cover the costs incurred by the buyer. These include the survey fee and the solicitor’s fee.

As well as the financial costs you will incur, there is also the chance that estate agents will be wary about working with you. They don’t get paid when transactions fail so they might be reluctant to represent you again.

Therefore, be absolutely certain that you want to sell your property before exchanging contracts so as to avoid any penalties.

How to speed up exchange and completion

One way to speed up exchanging contracts and completion is to carry out the processes for both on the same day. But as this isn’t always advisable, there are other ways to speed up the process.

Firstly, make sure you respond to requests for information quickly. If you are slow to respond to your conveyancer’s request, then the house-moving process will naturally slow down as a consequence.

Secondly, be sure to stay in regular touch with your conveyancer and estate agents. You may need to hurry them along if they are dragging their feet, or you may need to check for any issues that you can help resolve.

It will also help if you can agree on a completion day at an early stage as this will give everybody a target to work towards.

Tips to speed up the process for buyers

- Provide your conveyancer with everything they need from you, including the paperwork related to your mortgage offer and the monies required for property searches

- Make sure your deposit funds are accessible to your solicitor when you are getting close to the exchange date

- Choose a mortgage broker that can expedite mortgage offers

- Choose a trusted and experienced conveyancer

- Don’t go on holiday during the final stages of exchange and completion

- Sign the contract on the same day you receive it

Tips to speed up the process for sellers

- Gather the paperwork for your property early, such as receipts for any work that has been carried out and documentation relating to electrical and gas certification

- Hire the services of a solicitor before you are made a formal offer, as they will be able to get the title deed from your mortgage lender and prepare the sale contract at an early stage

- Choose somebody you can trust to carry out the conveyancing process

- Respond to requests for information in a timely manner

- Complete the fixtures and fittings/property forms as soon as you receive them

- Sign the contract on the same day you receive it

- Be accessible, even if this means postponing your holiday plans

What should the estate agent be doing during all this?

The estate agent will:

- Liaise with each party to make sure the transaction is going along smoothly

- Update the buyer and seller with information pertaining to the transaction

- Use software that gives the buyer and seller a login page to check for updates about the transaction (not all estate agents have this)

- Help to manage any problems that may arise during these final stages

Buyers: What needs to happen before I can exchange?

As a buyer, you must make sure:

- You receive a mortgage valuation from your lender and get approved for an official mortgage offer

- You have the money needed for your mortgage deposit

- Your deposit funds are cleared with your legal company

- You sign the sale contract

- You sign the deed of transfer (this isn’t always necessary if the seller has already signed it)

- You arrange buildings insurance for the property

- You agree to a completion date

Your conveyancer must:

- Have possession of the deed of transfer and the signed contract

- Be in possession of your deposit

- Check for any issues on the property survey

- Confirm (and have possession) of your mortgage offer

- Be in possession of your buildings insurance policy

- Prepare a completion statement (the document that itemises the financial transactions related to the house sale)

Sellers: What needs to happen before I can exchange?

As a seller you must:

- Respond to all enquiries by your conveyancer

- Provide all documentation required (such as warranties and gas certifications)

- Sign the contract and transfer of title

- Agree on a completion date

Your conveyancer must:

- Be in possession of all necessary paperwork, including the signed contract and transfer of title document

- Check to see that the buyer’s deposit has been lodged with their legal company

- Have an estimate of the mortgage redemption costs (outstanding balance and fees)

How do solicitors & licensed conveyancers exchange contracts?

In the past, solicitors and conveyancers would meet up in person to exchange contracts but these days, they are more likely to use the telephone.

During their conversation, they will agree to and confirm the terms of the contract. They will also make sure the required funds and documentations are in place.

Once they have confirmed and agreed to all this, the exchange of contracts will take place.

What is the process?

- The solicitor at the bottom of the property chain will contact the next one up and confirm that they have the signed contract and deposit in their possession

- The same solicitor will confirm a time for the exchange with the other legal representative

- The previous steps will take place between the other solicitors in the property chain

- The exchange will be confirmed down the chain to each legal representative

- If everybody is in agreement, the exchange will take place (if there are any issues, the exchange process will begin again the following day)

How long does it take to exchange contracts on the day?

It depends on how many people are in the property chain. If there is only one buyer and seller, then it will take no time at all. But if there are several people in the chain, it could take all day due to the number of mortgage companies and legal firms involved.

Why might the exchange not happen on the day it’s supposed to?

A delay might happen if there is a holdup with any paperwork or mortgage deposit funds, or if a solicitor or their clients aren’t contactable for any reason. A delay might also occur if the solicitor isn’t a very good one so it’s wise to do your research before picking a legal representative to minimise the possibility of something going wrong on exchange day.

What happens between exchange and completion?

Once the buyer and seller are legally bound to the transaction, the following will occur.

Who does what?

Below we look at what the buyer, buyers conveyancing, seller, and the sellers conveyance must do between the exchange of contracts and completion day.

Buyer:

- Arranges removal service

- Starts packing

- Contacts their utility companies and broadband suppliers about their impending move

Buyer’s conveyancer:

- Confirms the transfer of mortgage funds with the mortgage lender

- Checks terms on the lease (in the case of leasehold property)

- Draws up the completion statement

Seller:

- Arranges removals

- Starts packing

- Leaves a set of keys with their estate agent

Seller’s conveyancer:

- Confirms the mortgage redemption amount with the lender

- Draws up the completion statement

How long is it between exchange and completion?

Completion dates are typically within 14 days after the exchange of contracts but there can be a longer gap if:

- The buyer is in rented accommodation and they need to give notice to their landlord

- The property is a new build and building work isn’t finished

- The seller hasn’t secured their next property purchase

- A mortgage offer has expired

What happens on completion day?

The buyer’s funds are transferred to the seller’s conveyancer. At this point, the transaction is complete and ownership transfers and the seller must vacate the property.

What can cause delays on completion day?

Delays can be caused if:

- There is a holdup with the transfer of monies

- The seller hasn’t been able to vacate the property

- There are problems with the removal process

What happens if completion doesn’t take place?

As both the seller and buyer are legally bound to a contractually agreed date, they will be in breach of contract if they cause a delay to happen.

If the buyer fails to complete, they will be served with a notice that tells them they have 10 working days to complete before the contract is revoked. After this time, the seller has the right to a) pursue the buyer for financial compensation, and b) resell their property to somebody else.

If the seller fails to complete, they are liable for the buyer’s costs. They must also return the deposit paid to them. The buyer has the right to rescind the contract if it hasn’t been revoked already.

What happens after completion?

Below we look at what happens on the day off and after completion day and who does what.

Who does what?

Below we look at what the buyer, buyer conveyancing, seller, and sellers conveyancer must do on and after the day of completion.

Buyer

- Receives the keys to the property

- Checks that everything in the property is in order (as agreed in the contract of sale)

- Changes the locks

- Sends meter reading to their utility companies

- Lets their contacts know their new address details

- Updates their driving licence and council tax details

Buyer’s solicitor

- Transfers the deposit to the seller’s solicitor

- Registers the title deed with the Land Registry

- Submits the Stamp Duty Land Tax return and arranges for Stamp Duty to be paid to the HMRC

- Sends the buyer the Title Information document and SDLT5 certificate as evidence of Stamp Duty paid

Seller

- Takes the final meter readings

- Vacates the property

- Hands keys over to the estate agent

- Updates their driving licence and council tax with new address information

Seller’s solicitor

- Pays the estate agent’s bill

- Receives monies owed to them

- Redeems seller’s mortgage

- Pays monies owed to the seller

What is the buyer’s completion statement

The buyer’s solicitor will give them a statement that itemises all the financial transactions that have taken place (and that are still required) during the exchange and completion process.

It will include:

The total amount the buyer will pay the seller on completion

- Purchase price

- Additional payments that have been agreed upon

Fees, taxes, and charges

- Stamp Duty Land Tax

- Property search fee

- Land Registry fee

- Fees for pre-completion and identity checks

- Solicitor fees

Monies already paid/received by the legal company

- Exchange of contract deposit

- Mortgage advance

This isn’t a definitive list of what to expect on the statement as other fees may also be required.