A Guide to Debt Consolidation Mortgages & Remortgages

Home » How To Get A Mortgage » A Guide to Debt Consolidation Mortgages & Remortgages

Understanding Debt Consolidation Mortgages

Debt consolidation mortgages are a financial strategy that allows homeowners to consolidate their debts into their mortgages. This approach can simplify your finances by merging multiple payments into a single monthly mortgage payment. It can also potentially reduce your overall monthly outgoings, making your debts more manageable. Read on to learn how to get a mortgage for debt consolidation.

What is a Debt Consolidation Mortgage?

Mortgages to enable debt consolidation allow you to consolidate unsecured debts into one mortgage payment, eliminating multiple creditors and potentially lowering monthly outgoings. By consolidating debts under one loan agreement, they provide simplified financial management while potentially cutting monthly expenditures.

How Does a Debt Consolidation Mortgage Work?

The process of getting a debt consolidation mortgage involves several steps:

First Step in Assessing Debts: Step one is to take an inventory of all existing unsecured debts such as credit cards, personal loans, and bank overdrafts.

Seek expert advice from an advisor: Before making any decisions, it is wise to consult a mortgage advisor. A knowledgeable mortgage expert can offer tailored guidance that best addresses the potential benefits and risks associated with consolidating debt using refinancing mortgages.

Apply for a Mortgage: Next, it is important to apply for a large enough mortgage or remortgage loan to cover both your current mortgage and any outstanding debts.

Pay off your debts: Once your home mover mortgage or remortgage loan has been approved, use its proceeds to settle other outstanding debts.

Make Regular Payments: After taking out a new mortgage to cover both debts, make regular payments on it as prescribed by your new loan agreement. This should now include paying any prior debt that was unsecured.

Mortgages for debt consolidation can be complex processes and should only be undertaken after due consideration has been given. Before proceeding with any such decision, professional advice should always be sought from an experienced mortgage broker before taking action.

Debt Consolidation for Home Movers

Moving home can be an ideal time to consolidate debts. Doing this involves taking out a larger mortgage on the new property to cover both its purchase price and any existing liabilities.

How Does it Work?

When selling your home, the proceeds are used to pay off your existing mortgage and any leftover equity can then be put toward purchasing another one. Any excess funds may then be used toward repaying other debts.

By consolidating your debts into one mortgage, it may help simplify your finances and lower monthly repayments – though keep in mind that your new mortgage payments may increase and you’ll pay off the debt over a longer period.

Things to Consider

Before consolidating debts when moving home, several considerations must be taken into account:

Affordability: Can you afford the higher mortgage payments? Make sure that you can meet your new monthly repayments comfortably to protect the value of your home.

Interest Rates: Your new mortgage could offer lower interest rates than existing debts, potentially saving money over time. But this might not always be true so it is wise to compare rates prior to making your decision.

Longer Repayment Terms: Though consolidating debt into your mortgage may reduce monthly repayments, its longer repayment term means the total amount repaid may increase over time.

Home Equity: For consolidated debt to work effectively, sufficient equity must exist in your home. Without enough equity available to borrow against, consolidating may not be possible.

Prior to making any important financial decisions, it’s advisable to seek expert guidance. A mortgage advisor can assist in understanding all potential benefits and risks involved as well as offering guidance throughout the process.

The Mechanics of a Debt Consolidation Remortgage

When completing a Remortgage for Debt Consolidation, you’re effectively replacing your current mortgage with a new mortgage by releasing equity to raise funds to consolidate your debts.

Factors to Consider Before Remortgaging

Before making your decision to remortgage, it’s essential to carefully consider these factors:

- Equity: When consolidating debt, sufficient equity in your home must exist to cover its total amount.

- Interest Rates: Your new mortgage should feature an interest rate lower than the average interest rate on existing debts.

- Fees: Remortgaging may incur fees such as early repayment charges on your current mortgage and arrangement fees for your new one.

- Long-Term Costs: While refinancing may reduce monthly payments, it could increase your total debt repayment amount as you will spread payments over a longer period.

- Your Credit Score: When applying for a remortgage loan, having good credit scores can greatly enhance your ability to secure competitive terms and interest rates – otherwise remortgaging can become less beneficial than before. Low scores could even result in being offered higher interest rates that make remortgaging less desirable in terms of both fees and returns.

Is a Debt Consolidation Mortgage Right for You?

Many people remortgage for home improvements, it’s not too dissimilar, except you will use the funds raised to pay off unsecured debts to consolidate them into your mortgage for a more manageable monthly repayment. However, before choosing a debt consolidation mortgage, several key considerations must be considered, including equity available in your home, credit score, and the total amount you wish to borrow. Consult a mortgage advisor in order to make an informed decision and find an optimal loan program.

Pros and Cons of Debt Consolidation Mortgages

Like any financial decision, mortgages for debt consolidation come with their own set of advantages and disadvantages. Here are a few key points when making this choice:

Pros:

- Simplifying finances: Consolidating all your debts into one payment can simplify financial management.

- Lower monthly payments: Mortgages for debt consolidation can potentially reduce your overall monthly repayments.

- Reduced interest rates: Mortgage interest rates are generally more favourable as they are much lower compared to other forms of debt, so this could save you money in interest payments.

Cons:

- Long-term costs could be higher: Even though your repayments may be lower, extended repayment plans could cost more over time.

- Longer-term costs might be higher: Although your monthly repayments might be lower and more affordable in the short term, extended repayment plans could cost more over time.

- Your home could be at stake: If you fail to make mortgage payments on time, your existing lender could take possession and repossess your home.

The Role of Credit Scores in Debt Consolidation Mortgages

Your credit score plays a big part in the interest rates you will be offered when looking at mortgages to consolidate debt. Lenders use it to assess your creditworthiness and set an interest rate that best meets your needs; those with a higher credit score could qualify for lower rates while those with low scores may face more expensive rates, which may make these types of mortgages less beneficial overall.

Improving Your Credit Score

If your credit score is low, there are steps you can take to improve it before applying for zny mortgages to consolidate debt.

Pay Your Bills On Time: Any missed or late payments could have a devastating effect on your credit rating.

Reduce Your Debt: Your credit utilization ratio has an effect on your score; try to lower it as much as possible before applying for a remortgage loan.

Do not apply for new credit: Each time you apply for new credit can cause a small, temporary drop in your score; thus it would be wise to refrain from doing so before your remortgage application is submitted.

Check Your Credit Report For Errors: Errors on your credit report can wreak havoc with your score, so it’s in your best interests to review it free once per year and dispute any discrepancies you find.

Discover your true credit score and full report for free* with Checkmyfile.

Mortgage Advisor's Advice

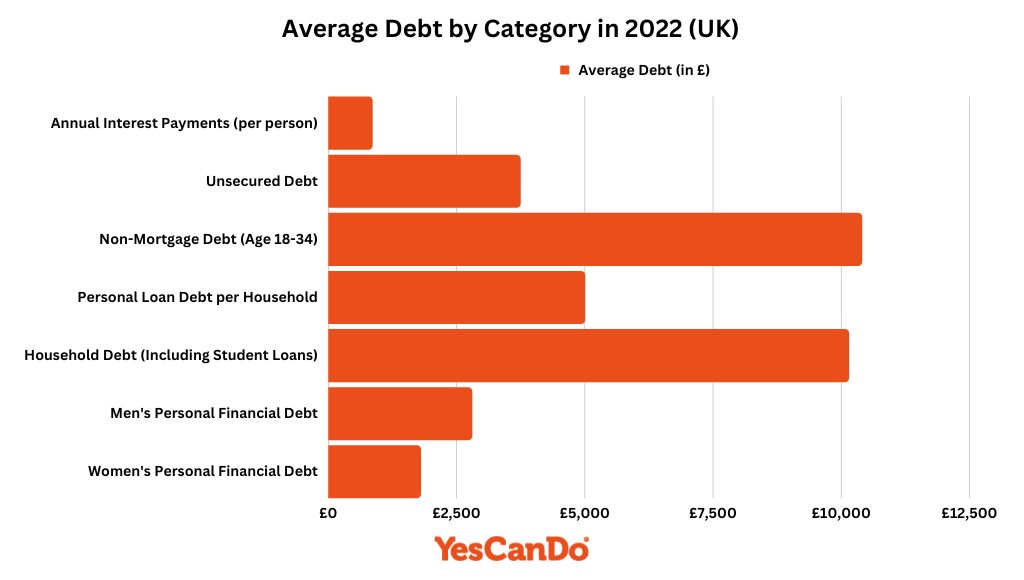

Average Debt by Category in 2022 (UK)

UK personal average total debt reached £33,410 by March 2022 – representing an increase from January 2020 by some £1,767; which equalled around 107% of average adult earnings.

Below is a breakdown of different types of debt and their UK average.

Alternatives to Debt Consolidation Mortgages

While mortgages to consolidate debt can be an effective means to repay debts, they’re not the only solution available to you – there may be several other avenues you should explore depending on your circumstances.

Secured Loans

Secured loans (also referred to as homeowner or second charge mortgages) provide an alternative consolidation of debt mortgage option if your poor credit prevents you from refinancing, or you’re currently locked into an expensive fixed-rate loan with early repayment charges. Like remortgages, though, secured loans put your home at risk if payments go unmade on schedule.

Further Advance

A further advance involves you needing to borrow money from your current mortgage lender. This additional borrowing is secured against your home, just like your original mortgage. This may be a good solution if your existing lender offers competitive interest rates, or if you wish to avoid the fees and charges associated with refinancing. To do so successfully, however, you will have to demonstrate to them that you can afford their increased repayments.

Personal Loans

If the amount of debt you need to consolidate is relatively low, consider taking out a personal loan as an unsecured debt option. These unsecured loans don’t depend on collateral such as your home; thus, possibly making personal loans a better solution. However, interest rates and monthly payments could be higher than with secured loans such as mortgages.

Credit Card Balance Transfers

If your debt consists mainly of credit card debt, a balance transfer may offer relief. This involves shifting any outstanding balance from one credit card with high-interest rates to one that offers lower or even 0% rates for an agreed-upon period – giving some breathing room while helping to repay the debt faster. But it requires discipline; aim to clear your balance prior to when this period ends as interest will likely resume again afterwards.

Each option has its own set of advantages and disadvantages; which one best suits your individual circumstances will depend on professional advice being sought prior to making any definitive decision. Before making an important decision for yourself, always seek expert opinion first.

Helping my customer consolidate unsecured debt

Conclusion

Consolidating debt mortgages can be an effective means of controlling and reducing debts; however, not every remortgage may suit every person. Therefore it’s vital that you carefully consider all relevant aspects before applying for any mortgage borrowing.

How a Mortgage Broker Can Help

Mortgage brokers can be invaluable resources when considering consolidating debt mortgages. They can help you understand potential benefits and risks, guide the application process efficiently and find you the ideal mortgage deal tailored specifically to your circumstances. At YesCanDo Money’s fee-free service, we provide expert advice without incurring additional expenses; so our mission is to help make smart financial decisions and the best remortgage deal!

Get a mortgage with the help from YesCanDo

- FEE-FREE mortgage support and advice

- We submit the mortgage application for you

- Team of expert online mortgage advisers

- Amazing communication via WhatsApp, email and SMS.

- Access to the whole residential mortgage market

Frequently Asked Questions: Debt Consolidation Mortgage FAQs

Can a mortgage be used to pay off debt?

Yes, a mortgage can help pay off debt through consolidation. This involves taking out a new mortgage that covers both existing loans and any outstanding debts so you can quickly repay these and then make one monthly payment toward your new mortgage.

Does debt consolidation pay off debt?

Consolidating debt doesn’t erase debt, but it can make it simpler. Consolidating multiple loans into one payment usually with lower interest rates can lower monthly payments and ultimately save money over time depending on the term.

Can I remortgage to consolidate debt?

Yes, remortgaging to consolidate debt is a common strategy. It involves replacing your existing mortgage with a new one that includes your other debts. This can simplify your repayments and potentially reduce your monthly outgoings.

Can I take equity out of my house to consolidate debt?

Yes, if your home has enough equity for refinancing release some of its equity and use it to pay off other debts. This is known as a consolidation of debt remortgage.

Can I remortgage with bad credit to pay off debt?

While it can be more challenging, it is possible to remortgage with bad credit. However, you may face higher interest rates or stricter lending criteria. It’s advisable to speak to a mortgage advisor to explore your options.

Can you get extra mortgage to pay off debt?

Yes, a larger mortgage may help consolidate your debts. This involves borrowing more than your current mortgage balance and using those extra funds to pay off other debts.

SPEAK TO A MORTGAGE ADVISOR

Let us know what the best time is for us to call you. We will get one of our mortgage advisors will be in touch to talk through your situation and available options.

OR FILL IN OUR FORM

"*" indicates required fields